Steel Processing Market Growth Driven by Construction and Automotive Demand 2030

Global Steel Processing Market Outlook 2024-2030: Trends, Dynamics, and Opportunities

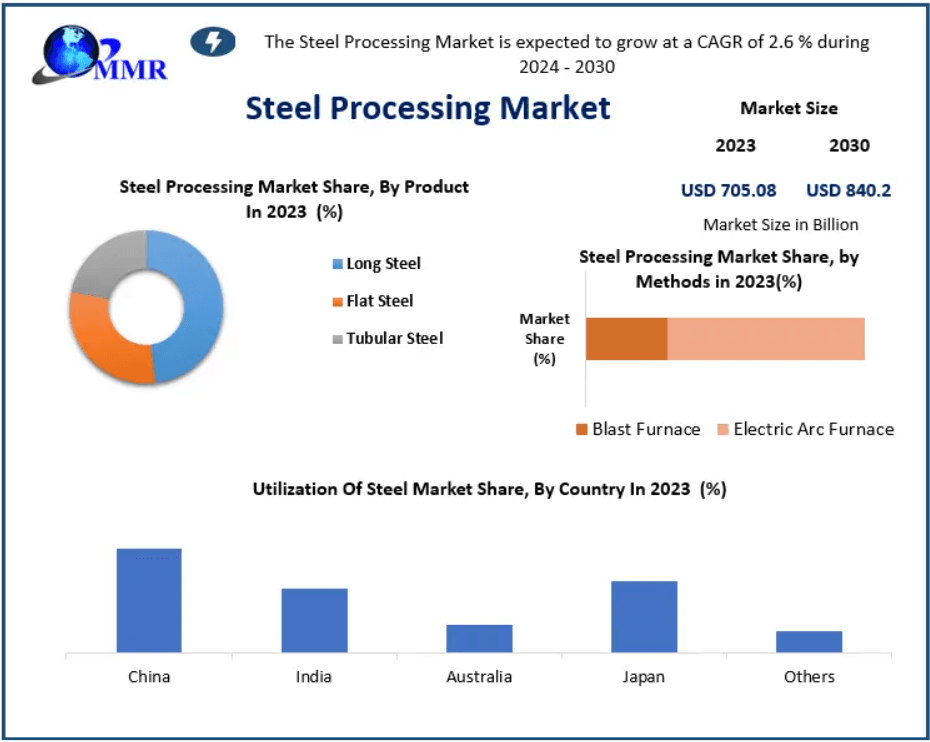

The Global Steel Processing Market was valued at USD 705.08 Billion in 2023 and is projected to reach approximately USD 840.2 Billion by 2030, growing at a CAGR of 2.6% during the forecast period. Steel processing, the critical process of transforming raw iron into high-quality steel products, plays a vital role across multiple industries, including construction, automotive, machinery, and infrastructure.

Download a Free Sample Report Today:https://www.maximizemarketresearch.com/request-sample/35216/

Understanding Steel Processing

Steel processing involves converting raw steel into finished products suitable for industrial use. The primary methods include blast furnaces and electric arc furnaces, which produce a wide range of products such as rebars, beams, sheets, and specialized alloys. The market covers the entire value chain—from sourcing iron ore and scrap metal to producing finished steel components for end-use industries.

Market Drivers

The steel processing market is driven by strong demand from the construction and automation sectors:

Construction Growth: Rapid urbanization, infrastructure projects, and residential and commercial developments are fueling the need for structural steel products like rebars, beams, and prefabricated components. Prefabricated steel structures offer enhanced durability and efficiency, contributing to increased market adoption.

Automation and Manufacturing: Advanced machinery, robotics, and industrial equipment rely heavily on processed steel for strength, flexibility, and longevity. Innovations in manufacturing technology improve efficiency, reduce material waste, and make steel more competitive compared to alternatives like aluminum and plastic.

Sustainability Trends: Approximately 70% of steel in the U.S. is recycled, demonstrating steel’s closed-loop production cycle. Sustainable steel practices reduce environmental impact, aligning with global carbon reduction initiatives and regulatory frameworks like the EU Emissions Trading System (EU ETS).

Market Restraints

Despite its growth, the market faces challenges:

Raw Material Costs: Fluctuations in iron ore and scrap metal prices directly impact manufacturing costs and profit margins for steel processors.

Economic Volatility: Steel demand is closely linked to economic cycles. Infrastructure and automotive projects often slow during recessions, leading to reduced production and revenue.

Download a Free Sample Report Today:https://www.maximizemarketresearch.com/request-sample/35216/

Market Segmentation

By Type:

Carbon Steel: Dominated the market with a 33.5% share in 2023. Its versatility and high strength make it ideal for automotive parts, machinery, and construction materials.

Alloy Steel: Gaining traction due to specialized applications in high-performance machinery and infrastructure.

By Product:

Long Steel: Majorly used in construction, bridges, highways, and railways, long steel products drive the majority of demand.

Flat Steel and Tabular Steel: Used in automotive bodies, industrial equipment, and metal products, supporting market diversification.

By End User:

Building & infrastructure

Automotive

Mechanical equipment

Metal products

Transport & logistics

Electrical & domestic appliances

Regional Insights

Asia-Pacific: The largest market with a 41.5% share in 2023, driven by rapid industrialization, population growth, and abundant raw materials. China and India lead the region’s steel production, investing heavily in advanced technologies and manufacturing facilities.

North America: Emerging as the fastest-growing region due to high demand in the automotive industry and emphasis on lightweight, high-strength steel solutions. Domestic trade policies favor local steel production.

Europe: A mature market with a strong focus on sustainable practices, advanced manufacturing capabilities, and specialized steel applications.

Competitive Landscape

Key players in the global steel processing market are actively pursuing mergers, acquisitions, and strategic partnerships to expand their market presence:

Asia-Pacific: China Baowu Steel Group, Baosteel Group Corporation, POSCO Holdings, Angang Steel Company, Tata Steel, NACHI-FUJIKOSHI, Daido Steel, Nippon Steel & Sumitomo Metal Corporation, JFE Holdings, Jianlong Group, Shougang Group, HBIS Group.

Europe: Arcelor Mittal, Sandvik AB, ERASTEEL.

North America: Kennametal Inc., Hudson Tool Steel Corporation.

Latin America: Gerdau SA.

Download a Free Sample Report Today:https://www.maximizemarketresearch.com/request-sample/35216/

Notable Recent Moves:

In 2023, China Baowu partnered with Shandong provincial authorities to acquire a 49% stake in Shandong Iron & Steel Group, strengthening its market dominance.

Tata Steel, India, expanded through acquisitions of Neelachal Ispat Nigam Ltd (NINL) and NatSteel, consolidating its presence in steel production and long product manufacturing.

NSK Ltd and ThyssenKrupp AG formed a joint venture to advance automation and precision steel technology.

Future Outlook

The steel processing market is expected to continue its steady growth, driven by:

Infrastructure development in emerging economies

Increasing automation and industrial machinery production

Innovation in eco-friendly and high-strength steel solutions

Government incentives for domestic production and export

With Asia-Pacific leading global production, North America accelerating technological adoption, and Europe focusing on sustainability, the steel processing market is poised for robust and strategic expansion in the coming years.

Appreciate the creator